Industrial Market Rebounds: Stronger Demand Signals Stabilizing Logistics Sector Heading into 2026

After a turbulent start to 2025, the U.S. industrial real estate market regained momentum in the second half of the year, signaling that businesses are beginning to adjust to shifting economic conditions and policy uncertainty. New projections from the NAIOP Industrial Space Demand Forecast suggest the sector is entering a period of stabilization, with demand expected to steadily improve through 2026 and into 2027.

According to the forecast, net absorption of industrial space totaled 128.7 million square feet during the second half of 2025, reversing earlier weakness that included negative absorption in the second quarter. The rebound indicates that occupiers—particularly those tied to logistics, distribution, and manufacturing supply chains—are regaining confidence following a period of uncertainty tied to interest rates, tariff policy, and broader economic volatility.

By the end of 2025, total net absorption reached 168.3 million square feet, a notable improvement over projections made earlier in the year.

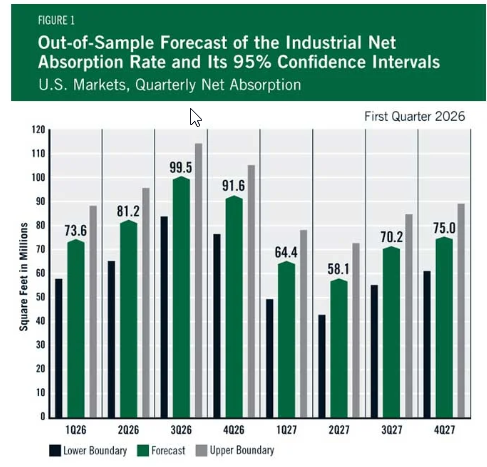

Looking ahead, the outlook suggests stronger demand as businesses operate in a more predictable environment. The NAIOP forecast projects that industrial space absorption will rise to 345.9 million square feet in 2026, before moderating slightly to 267.7 million square feet in 2027. While still below the historic peak of 630.7 million square feet absorbed in 2022, the forecast signals a return to healthier, more balanced market conditions.

Supply Outpaced Demand in 2025

Despite improving demand, the industrial market continues to absorb a large wave of new supply delivered during the recent development boom. According to CoStar data, industrial deliveries in 2025 exceeded net absorption by roughly 220 million square feet, pushing the national vacancy rate up to 6.9%, compared with 6.2% at the end of 2024.

The increase in vacancy reflects a classic cycle following a period of aggressive development. Developers responded to extraordinary demand during the pandemic-era logistics surge, but as new facilities entered the market, leasing activity temporarily lagged behind.

As a result, market conditions are gradually shifting toward equilibrium. Analysts expect average industrial rents to remain relatively flat across many markets in the near term, as landlords work to absorb newly delivered inventory.

However, the broader trend suggests that supply and demand are moving closer to balance as leasing activity strengthens.

E-Commerce and Consumer Spending Continue to Drive Demand

Several structural drivers continue to support industrial real estate demand, particularly the ongoing growth of e-commerce and consumer spending.

Retail sales excluding gasoline stations increased 4.2% year over year in December, while online retail sales grew 5.1% during the third quarter. E-commerce now represents 16.4% of total retail sales, slightly above the previous record set during the pandemic.

That steady shift toward online purchasing continues to reshape supply chains, driving demand for modern logistics facilities, fulfillment centers, and distribution hubs.

Logistics providers and third-party distribution firms remain among the most active industrial tenants. Many occupiers are also seeking to upgrade from aging warehouse stock to newer buildings designed for higher throughput, automation integration, and improved logistics efficiency.

This trend is particularly visible in major logistics corridors and fast-growing regional distribution markets where the supply of modern space remains constrained.

Economic Conditions Improve After Early-Year Volatility

Broader economic conditions also improved as 2025 progressed.

After contracting during the first quarter, the U.S. economy returned to growth, with real GDP expanding at annualized rates of 3.8% in the second quarter and 4.4% in the third quarter. The Federal Reserve Bank of Atlanta has projected 3.6% growth for the fourth quarter, suggesting the expansion continued through year-end.

Several policy events contributed to early volatility. New tariff policies introduced uncertainty for manufacturers and importers, slowing investment decisions and industrial leasing activity during the second quarter.

Later in the year, a 43-day federal government shutdown—the longest in U.S. history—delayed economic data releases and added further uncertainty to the market environment.

Despite those disruptions, the labor market remained relatively stable, with the unemployment rate at 4.3%.

Consumer Sentiment Remains a Wild Card

While economic indicators have generally been positive, consumer sentiment tells a different story.

The University of Michigan’s consumer sentiment index measured 57.3 in February 2026, a decline of more than 11% from the previous year and close to levels last seen during the 2008 financial crisis.

This divergence between economic fundamentals and consumer perception has become one of the key uncertainties facing the industrial market.

If consumer confidence weakens further and spending slows significantly, demand for logistics and distribution facilities could decline quickly. However, consumer spending has remained relatively resilient so far, allowing industrial demand to continue growing despite pessimistic sentiment readings.

Inflation and Labor Trends Shape the Outlook

Inflation has cooled but remains above the Federal Reserve’s long-term target.

The core Consumer Price Index increased 2.5% over the past year, suggesting that borrowing costs may remain elevated longer than many market participants had expected.

Higher interest rates could slow new industrial commitments or development starts, though they may also help prevent another oversupply cycle.

Meanwhile, labor market conditions have begun to soften. Job growth slowed dramatically in 2025, averaging 15,000 new jobs per month, compared with 168,000 monthly jobs added in 2024.

Because employment trends directly influence consumer spending and supply chain activity, the direction of the labor market will be a critical factor shaping industrial demand in the coming years.

Forecast Model Signals Stabilization

The NAIOP Industrial Space Demand Forecast relies on a sophisticated statistical model developed by economists Hany Guirguis of Manhattan University and Joshua Harris of Fordham University.

The model evaluates more than 40 economic and real estate variables, including manufacturing output, employment levels, GDP growth, imports and exports, transportation activity, and historical absorption data.

Using techniques such as Kalman filtering and exponential smoothing, the model accounts for seasonality and shifting economic relationships, allowing the forecast to adapt to evolving market conditions.

Key leading indicators include the Federal Reserve’s Index of Manufacturing Output and the Purchasing Managers Index from the Institute for Supply Management, both of which provide insight into broader supply chain activity.

What It Means for Industrial Development

For developers, investors, and construction firms, the forecast points to a market transitioning from rapid expansion to measured growth.

The extraordinary industrial boom of 2020 through 2022 has cooled, but the underlying drivers of logistics demand—e-commerce, supply chain restructuring, and population growth—remain firmly in place.

Over the next several years, the market is expected to shift toward higher-quality logistics facilities, modernization of aging inventory, and strategic regional distribution networks.

For fast-growing regions such as the Carolinas and the broader Southeast, those trends could translate into continued demand for large-scale distribution facilities, advanced manufacturing logistics hubs, and modern warehouse space tied to e-commerce supply chains.

While economic uncertainty remains a factor, the data suggest that the industrial sector is moving toward a more stable—and sustainable—growth cycle.

And for an industry that spent the past several years racing to keep up with demand, stabilization may be exactly what the market needs.