With War Raging and Oil Surging, What is the Economic Outlook?

With a war raging in the Middle East, trade wars at play elsewhere, crude oil prices rising above $100 a barrel, the White House threatening a Cuba takeover and U.S. saber rattling directed toward Greenland, economic policy uncertainty is peaking and major investment decisions are being put on hold. Is there anything meaningful that we can say about the prospects for the 2026 U.S. economy?

Perhaps the best we can do is get a handle on a baseline and identify how the nation and our region are positioned to handle what seems to be coming. With the help of data maps for the nation, I will lay out where we stand now. Doing so may help individual decision makers determine what may happen later. Of course, the greater our current strength, the better we can deal with difficult challenges to be faced.

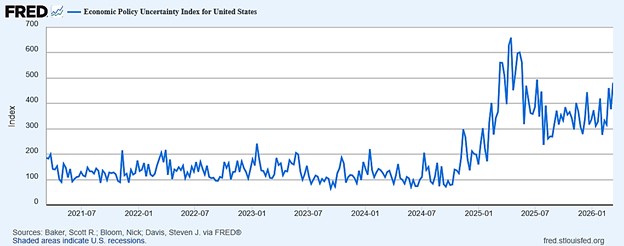

First, consider Figure 1, which reports a weekly estimate for Economic Policy Uncertainty for the last five years. Notice the long period of stability that ended in early 2025. Then, note the spike that occurred in April 2025 when Trump unveiled his trade war plans. This action started a turbulent period of changing tariffs that were used for multiple political purposes. Trump’s initial effort was invalidated by a Supreme Court decision, which then brought changes in White House tariff justification, but the tariffs continue, and they are at least partly a tax on the American people. Since then, new boulders of uncertainty have dropped regularly into the economic seascape, and investment decision makers have been challenged to determine how to respond.

Now, consider inflation. Estimates for February year-over-year CPI inflation just received indicate the pace remains at 2.4%. This is well above the Fed’s 2% target, but a lot better than it was a year ago. But with high oil prices now rattling markets and increased deficit spending, the likelihood of a Fed-softening of interest rates is headed toward zero. More Fed money creation and war-fed demand for resources will bring more inflation. We should look for 2.7% CPI inflation toward the end of this year.

What about GDP? Well before the U.S. invasion of Iran, U.S. GDP growth was hitting 4.4%, but early estimates of 4th quarter GDP growth came in at a cool 1.4%. Though already weak at 1.4%, on March 13, the number was revised downward to 0.7%. In a word, we have a cooling economy. Things may turnaround in the months ahead, but what we see right now does not look like America’s golden age. In February the U.S. economy lost 92,000 jobs. With hardly any overall 2025 employment growth, healthcare and educational services were America’s high job-growth sectors, and they are funded primarily with taxpayer money. So how can one square the earlier four percent real growth for an economy that shows hardly any employment growth? After all, GDP is produced by people!

Recalling that real GDP growth is determined by gains in total hours worked plus growth in labor productivity yields an answer. Productivity improvements generated by AI, record-setting new business formations, and investments in related power generation must be a major part of the explanation, and I expect this to continue. Productivity growth for third quarter was 4.9% and 2.8% in the 4th. By comparison, a year ago the value was 1.9%. Reductions in taxes and regulation may be contributing a positive nudge, too.

Building a Baseline

Prior to the Middle East war, estimates for GDP growth were being revised upward. In Table 1 I show quarterly real GDP growth estimates for 2026 for three forecast groups I regularly follow. It’s important to note that the Wall Street Journal and Wells Fargo estimates surfaced in January. The Philadelphia Fed’s forecast was produced in November 2025. The contrast between early and late is striking but commonly seen. As we think about building a mental economic baseline for assessing the current situation, we should note that no recession was expected by the forecasters, but the pace of output is much slower than the growth we saw in 2025’s third quarter. The reason? The forecasters indicate that they expect Trump’s tariffs to begin to bite. Now, we have the Middle East war taking a bite. Let’s pencil in a loss of 0.20% in real GDP growth across the next six months.

Table 1 | Real GDP Growth Forecasts

| 4Q-2025 (%) | 1Q-2026 (%) | 2Q-2026 (%) | 3Q-2026 (%) | 4Q-2026 (%) | |

| Philadelphia Fed | 1.1 | 1.6 | 1.7 | 1.9 | |

| Wall Steet Journal | 2.2 | 2.1 | 2.1 | 2.1 | 2.1 |

| Wells Fargo | 2.0 | 3.3 | 1.6 | 2.1 | 2.3 |

Sources: https://www.philadelphiafed.org/surveys-and-data/real-time-data-research/spf-q4-2025. November 2025. https://www.wsj.com/economy/economic-forecasting-survey-archive-11617814998?mod=article_inline January 2026. https://wellsfargo.bluematrix.com/docs/html/fd90201b-846c-4159-a345-b5f3ec4c9d21.html January 2026.

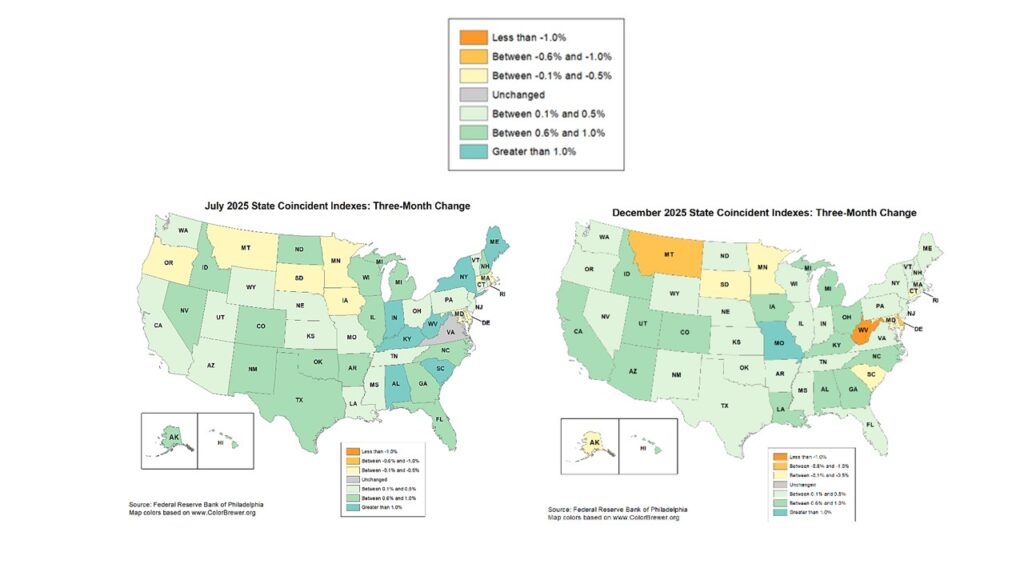

Things were slowing long before the start of the Iran war. We observe a slowing economy when we look at the change in state coincident indicators for the 50 states. In the next panel I show charts for July 2025 and December 2025. I note that December is not quite as brightly colored as July.

Looking at Geographic Patterns

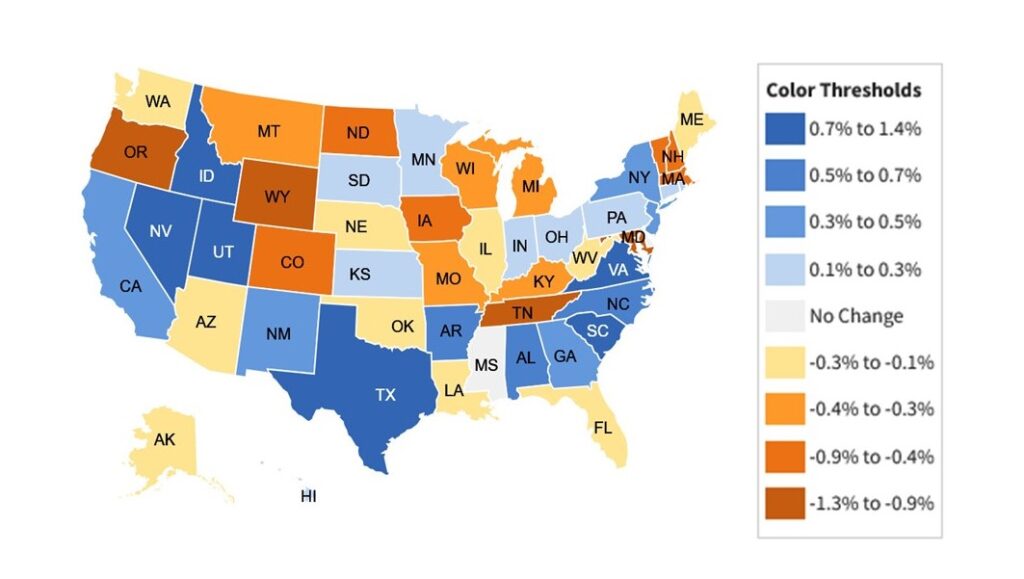

Let’s now look at 50-state data on employment growth, first for all industries, then for manufacturing, and finally for construction. The data I provide, just released by the Bureau of Labor Statistics, give growth estimates for 2025’s third quarter. As shown in Figure 3, most states were showing weak growth. The southeast, west, and far-west show strength.

The picture for manufacturing shown in Figure 4 is much bleaker. Just four of the 50 states show employment growth. There can be little doubt; the U.S. is a services economy. There can also be little doubt that efforts to stimulate manufacturing jobs with tariffs have had little effect.

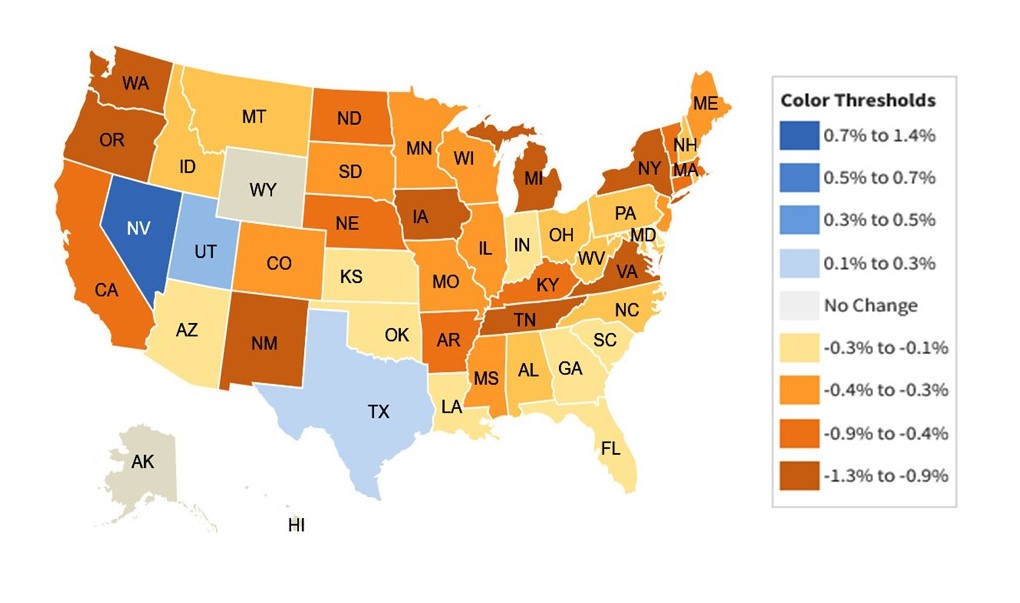

Finally, Figure 5 reports construction employment growth. Here we see widespread strength with the southeast again being one of the stronger regions.

Final Thoughts

As we think about building a baseline to use in determining how the nation and our region may be positioned to deal with war-based realities and uncertainties, it seems we have at least one positive force at play and multiple negative ones. AI and building the power generation to feed it are a green sprout to welcome. Higher energy prices, inflation and accompanying higher interest rates are negative forces to deal with. More volatile uncertainty will continue to becloud the situation. Bottom line? We should make it through 2026 a bit more bruised than otherwise, but we should not encounter a negative GDP-growth recession.

Let’s see what happens.