The Economy at Mid-year: Some Good News and Bad News

On June 25, the U.S. Department of Commerce delivered good news and bad news all in the same day. The good news came with an upward revision for first quarter 2026 real GDP growth. The final estimate rose from 1.6% To 2.1%. Once again, we are back running in the twos. (Recent real GDP growth was 2025: 2.1%, 2024: 2.4%, 2023: 3.4%, 2022: 1.3%.) At about the same time, the New York Fed’s Nowcast and Atlanta Fed’s GDPNow estimates for second quarter were resting at 2.7% and 2.5%, respectively. The readings suggest that despite the Iran war’s destruction and disruption of energy markets, the economy is in a mild growth spot, rocking along at a slow, but now normal, pace.

No, this isn’t evidence of a new golden age, as promised by Trump, but the data tell us the Great American Bread Machine still works, perhaps in spite of what Washington does to it. We must remember that GDP growth is determined by adding labor force growth to growth in labor productivity. Right now, there is zero labor force growth, driven by an aging population and immigrant deportation and with more immigrants due to be shipped out. Those two demographic trends will continue, so in spite of AI magic, we will have to become accustomed to low-level GDP growth.

Then, came the bad news. Inflation measured by the Fed-preferred Personal Consumer Expenditure Index came in with an annual rate of 4.1%. When food and energy were stripped away, the index still stood at 3.6%, well above the Fed-sought 2.0%, and far more than can be attributed to the attack on Iran.

Let’s take a closer look and see where the growth is coming from generally and how the construction industry is affected.

Where’s the growth?

The headlines shout out news about SpaceX, Nvidia, and massive AI-sponsored data centers. But these are not the major sources of U.S. GDP growth. In fact, railroad freight data tell us that we are experiencing record levels of rail shipments that cut across 15 of 20 national sectors. Manufactured goods are part of the growth picture. But agriculture is the leader.

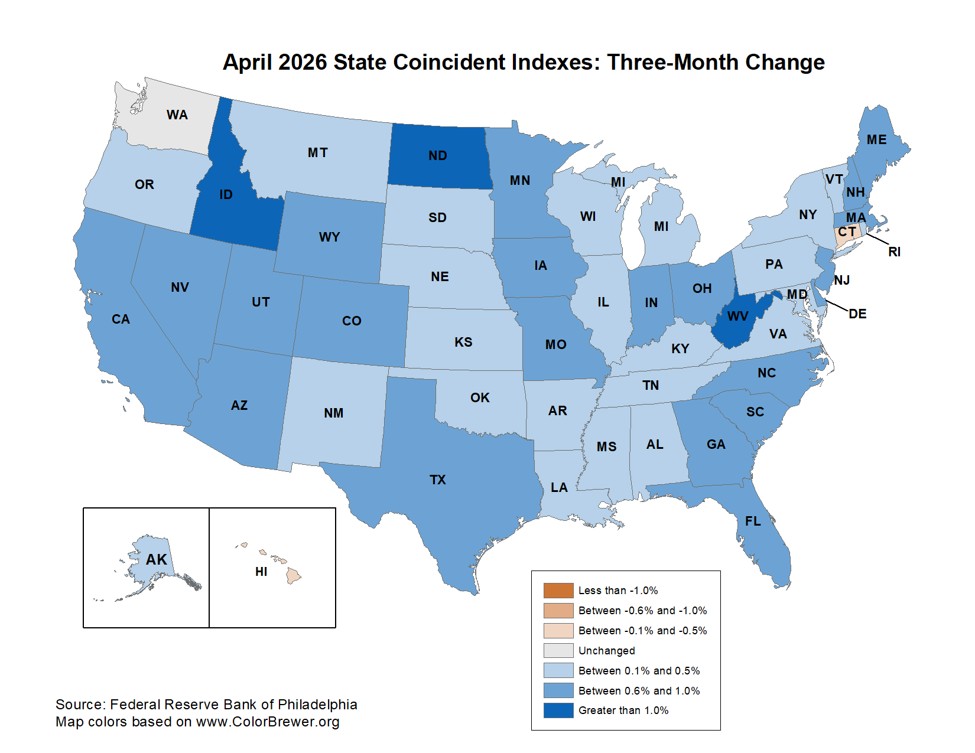

What about the geography of growth? The latest 50-state chart for coincident index growth by the Federal Reserve Bank of Philadelphia for May, shown below, reports widespread activity. Just four states, Connecticut, Kentucky, Alabama, and Hawaii, showed negative growth. This is one of the most positive pictures we have seen in a while.

Construction activity?

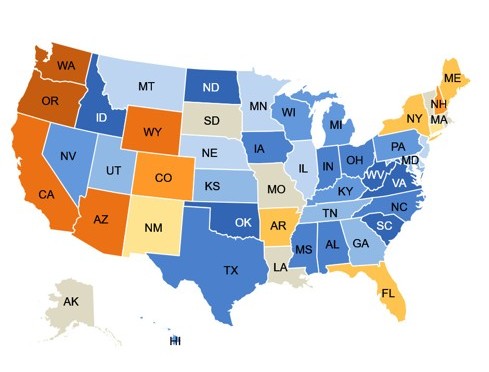

A quick look at construction employment shows wide-ranging differences across regions. In the next chart, BLS data on employment growth show East of the Mississippi River is by far the nation’s stronger half. With the exception of Florida, the South continues to be a stand-out region.

12-month percent change in construction employment, 12/24-12/25

Inflation and prices

Now let’s look closer at the ongoing 4.1% surge of inflation measured by the Consumer Expenditure Index that was mentioned at the beginning of the article. I noted that when energy and food are removed, there still remains an ongoing 3.6% inflation level. Clearly, there are two elements here. Let’s call the first one “foreign made.” The energy surge is clearly the result of the Iran war. Of course, the action was a decision made in Washington, but the surging relative price change was imported to our economy (and to all other economies) from abroad. The remaining 3.6% inflation component is “home made.” But let’s not get carried away with this nomenclature. We must remember that there can be no inflation where all prices taken together increase, unless the Fed increases the amount of money circulating in the economy.

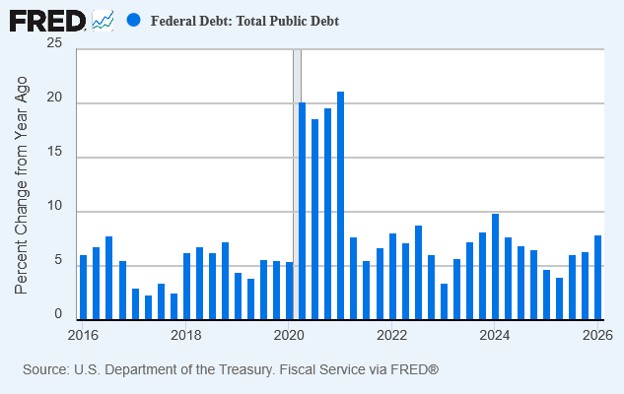

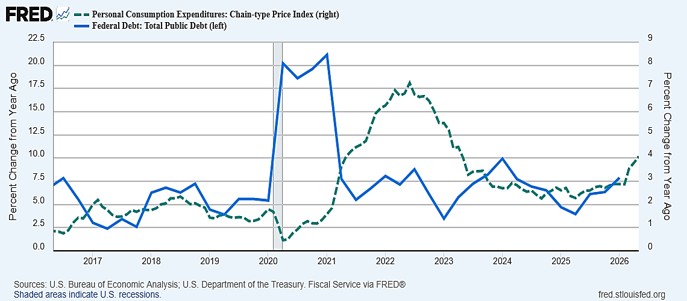

When the federal government sells bonds and prints money, the result is more dollars chasing a limited amount of goods and services available to us. All prices taken together tend to rise. That’s good ole American homemade inflation. Deficits and growth in government debt to fund them make it happen. Economist Jonathan Hughes called it the “government habit.”

Data on growth in public debt shown in the next chart tell us that in spite of federal layoffs and shutdowns, the Trump administration is maintaining the Hughes habit. The chart shows the explosion in debt that occurred when a lot of money was printed in association with COVID. This is followed by a chart that maps growth in federal debt into the Personal Consumption Expenditure Index. Note the 7.2% inflation that followed in June 2022. That surge of newly printed money was chasing goods in a shutdown economy. A close look at the most recent four quarters tells us that deficits are growing; this predicts that “home-made” inflation will continue apace.

Construction inflation?

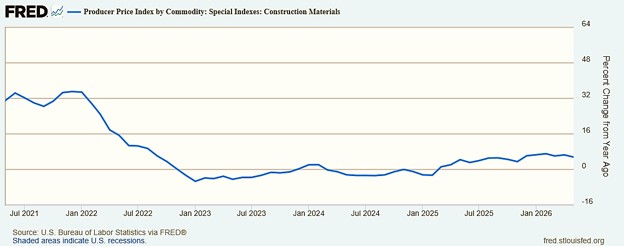

Inflation occurs unevenly across the economy. Consider the next chart, which shows growth in the Producer Price Index for construction materials. We certainly see positive movement, especially since January 2025; May 2026 shows a 5.8% annual increase, which is well above the overall 4.1% inflation rate.

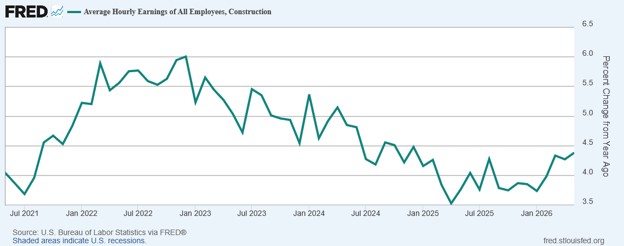

The effect of inflation on wages is another matter. As shown in the next chart, which shows year-over-year growth in construction wages, the growth rate was falling from 2023 through 2025. That changed. The rate of growth is now hitting 4.4% year-over-year. Wages increases are just slightly higher than the current rate of inflation.

Final Thoughts

As 2026’s first half closes, we may be comforted knowing that the Great American Bread Machine is again growing somewhat smoothly at better than a 2% annual rate. Not only that, but with growth distributed broadly across the 50 states. That’s the good news. Rising, almost run-away inflation is the bad news. And this is home-made, the result of the government habit that our political system seems unwilling to break. The better than 4% inflation we are dealing with is largely the result of actions taken by the federal government to provide us with more benefits than we are willing to pay for, and to do so with printing press money. The mixed-bag economy will continue apace, but as usual, the road ahead will be bumpy.